In recent years there have been a number of cases in which controlling shareholders have used the threat of delisting to force out minority shareholders at unfairly low prices. Years ago, we wrote about a Malaysian case here. That turned out to be a prelude to repackaging and relisting. The aggressor apparently found this so lucrative that he started a series of delistings and relistings. We prefer to invest in businesses where we are treated as long-term partners - and are unhappy about the way in which Fincantieri is trying to privatize its Singapore-listed subsidiary, Vard Holdings.

This has been a disappointment. Despite the dismal share price performance since Fincantieri took control, it has seemed operationally helpful, facilitating diversification after the severe downturn in oil & gas, assisting in keeping the yards busy and the skilled workforce as intact as possible, and broadening the pool of managerial talent.

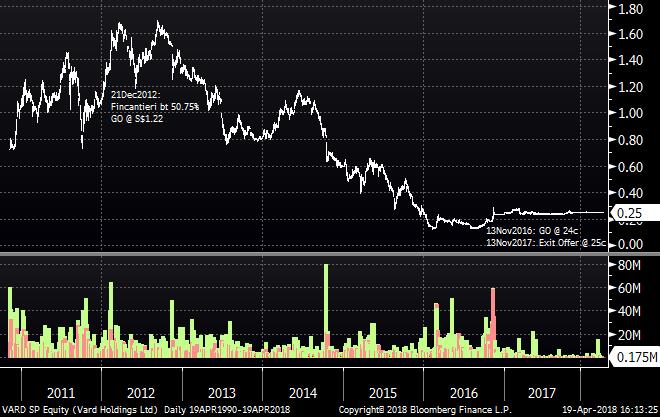

We understand why Fincantieri might wish to privatise Vard, now more integrated with its group operations. It bought 51% and made a general offer at S$1.22 per share in 2012. Now that Vard has survived the downcycle and its prospects are improving, we understand why Fincantieri has wished to buy as much as it can at 24c in 2016 and at 25c in 2017. We understand that the group operations are now more integrated: it would save costs and management time for Fincantieri if it controlled 100%. What we object to is being forced to sell at a price we consider unfair, and this may well happen under the current rules.

We therefore set out here our immediate recommendations to Vard shareholders, an important question, our recommendation to Fincantieri to save its reputation, and the general issues illustrated by this case.

To Vard shareholders:

urgent! EGM soon,

please vote against delisting

Shareholders of Vard Holdings, please note the EGM called for 30 April to vote on delisting, and ensure that you vote against. The timetable is unusually tight, and a high turnout of independent investors is required to keep the shares listed. The company's performance is improving as the cycle for its specialist shipbuilding turns up. Fincantieri wishes to take it private, at just 20% of the price at which it failed to get takeup for a general offer in 2012, and 15% of that year's shareprice high. (It was then widely owned as a yield stock: at that GO level, the historic dividend yield was 12%.) Keep it listed and wait for the upturn - or to be persuaded, uncoerced, by a fair exit offer.

The Independent Financial Adviser correctly describes the Exit Offer at 25 cents as NOT FAIR, but if the shares are delisted, many investors will be squeezed out rather than holding shares in an unlisted company, and that is very likely to take Fincantieri up to the 90% at which it can compulsorily acquire the rest. The free float is now less than 17%, and it requires 10% of the votes cast to veto de-listing. Therefore, at least 55% of ongoing investors must vote against delisting to avoid this fate, and the percentage turnout required will rise with each additional share that Vard manages to buy. No minority shareholder who has held on this long would vote for delisting: anyone wishing to exit could for most of the last 18 months have sold at the same price or better, and taken their money immediately. Ongoing shareholders clearly wish to hold on for the cyclical upturn which is already under way. The danger however is that many may not vote, if they do not hear about it in time, or fail to realise the urgency. Please publicise this, and urge shareholders to vote. (In the worst case, if the turnout is insufficient to block delisting, there will still be time to accept the exit offer, and then receive payment within seven days - so first, please vote to avoid delisting.)

Fincantieri has seemed to be trying to starve investors into submission, with an exceptionally prolonged period of uncertainty which has now lasted for a year and a half (a cheeky lowball general offer, creeper purchases, and yet another general offer at a mere 4% higher, although the fundamentals have improved by far more). As this lengthy period wore on, fresh interest in the stock was minimized by Fincantieri's threat of a later compulsory purchase. Even though the fundamentals have improved significantly, the share price has been capped by that threat. This has been dragged out for an inordinate length of time - and now the pace has suddenly been accelerated. The minimum permitted notice period has been given for the EGM, and a 328 page circular published, most of which relates to the Exit Offer (and why it is NOT FAIR! inadequate premium, a discount even to NAV, improving orderbook and fundamentals) - rather than what shareholders need to act on immediately, which is the EGM vote on delisting. The company is behaving as if delisting is certain, providing no 2017 annual report, and scheduling no AGM. This behaviour may confuse. Delisting is not inevitable. Vote for your right to hold, and to exit at a time and price of your choosing. Vote against coercion, and against delisting.

Question: - what is an "independent" director??

The Vard CEO Roy Reite is apparently deemed "independent for the purposes of making recommendations to Shareholders in respect of the Exit Offer", according to p.4 & 19 of Vard's circular on the delisting proposal. I find this extraordinary. He has worked for Vard for at least 19 years. Vard is a subsidiary of the aggressor. His career and his pension depend on Fincantieri. How can he possibly be considered unbiassed in this matter?

To Fincantieri:

Your leadership in Italy has left routine announcements in Singapore to the local financial adviser, and may have agreed to attempt privatisation without considering the details from the perspective of a long-suffering local investor. As the unfairness becomes apparent, there's an honourable option available: to refrain from voting the controlling block in the EGM, allowing the independent shareholders to decide (as in Hong Kong) if they wish the shares to remain listed, and a free choice on holding or selling. If Fincantieri wins the requisite majority on a free vote in the EGM, or can reach the 90% required for compulsory acquisition, fair enough. Offering a fair price for the remainder would make little difference to your average Vard cost, and you could leave Singapore markets with your reputation intact - rather than with an ignominious place in governance history, and a final taste of ashes and gall.

Issues, and possibilities of improvement:

1. Tweak the required voting percentages

A delisting proposal should be rejected if opposed by holders of 10% of the unconnected votes cast.

The controlling shareholder and connected parties should be disqualified from votes on delisting, as in Hong Kong

(rule 6.12 of

the Listing Rules). Under Singapore's present

rules, even if the independent shareholders who vote are

unanimous in rejecting the proposal, it may pass anyway unless the voting

turnout is unusually high.

Not voting does not mean the shareholders don't care!

Reasons for not voting include custodian paperwork delays,

postal delays, holidays,

hospitalisation, probate, dauntingly thick and confusing documents... the rules may have

been devised for an earlier era of mostly-local shareholders, holding

shares in their own names, with efficient

postal services, and usually at home.

In current conditions, achieving a high turnout with two weeks' notice may

be

challenging. If we snooze we lose. If others snooze, we may also lose - so if you know people who

own or have the voting authority for Vard shares, please ask them to vote too.

2. Timetable review

Timetables should be reviewed to ensure that the period of uncertainty

caused by the threat of delisting is not unduly prolonged. Vard's ability to

drag this out over a period of about

eighteen months has, in our view, depressed

the market price, and discouraged other buyers from entering,

precisely because of

the sustained threat of delisting and the risk of forced sale at a low price. No

threat,

no price depression. Short-lived threat, short-lived price impact

followed by normalisation. 18-month threat,

especially with the price both

underpinned and capped: brokers stop following, analysts drop coverage,

investors lose interest.

3. Documentation review

(i) On Vard's second offer, it should have

been required to set out the

timetable, agenda, and required majorities for

critical meetings promptly, rather than many months later.

Other information in the circular, such as the report of the Independent

Financial Adviser, could be allowed to follow later.

(ii) Are property valuation reports essential, or should the requirements for these

be tailored to the type of company?

Vard's circular contained detailed

descriptions and valuations of each of its dockyards around the world, a total

of 212 pages. I

inspected these with astonishment, thinking about the amount of work that must

have gone into

compiling them all, and the limited impact I envisage on anyone's

decision - indeed, I wonder how many people

will read them at this stage. (There's much more detail here than in the IPO prospectus or in annual reports,

when it might have been useful.)

With other

types of company, the property may indeed be key to the valuation, but assets

like these have a limited market and a business like this is all about the profits and

cashflows which the assets

can generate. If there were a possibility for windfall gains

from land use change, it would be good to ensure that all

shareholders had

relevant information, but perhaps in that case it could be provided more

succinctly?

(iii) The hundreds of pages of documentation in these categories relate to the

valuation of the business, and the

(lack of) merit in the Exit Offer, rather

than to the delisting vote which is more urgent, and which may make all

of that

irrelevant. Do readers find this confusing? Should it be separated, for

clarity?

(iv) Annual reports and standard information should be provided on the normal

schedule for as long as a company

is listed. (For example, Vard can see its

share register: the rest of us can see only the version from 13 months ago.)

AGMs, too, should be held as normal.

(v) Does the wording lead to confusion? Does the For/Against direction make a difference?

Are guidelines needed? I suspect it might elicit slightly different responses if the question were:

"Do you wish your shares to remain listed on the Singapore Stock Exchange"? rather than the more complicated

resolution presented for the EGM, which requires a negative vote for a positive outcome, and refers to a 'Voluntary

Delisting' although no independent investor should volunteer for it. A headline "Forced Delisting Proposal and Unfair

Exit Offer" would represent the situation accurately and alert investors to pay attention.

4. "Independent" directors

If a significant majority of independent votes cast disagrees with the

recommendation of the "independent" directors, the latter should be immediately disqualified from

serving as independent

directors of any Singapore company for a period of several years.

Vard's "independent" directors recommended investors to

vote for delisting, on logic I would summarise as follows. "Our bosses want to take the company private. We will

delist it. Then you will have no better choice than selling out at our price. It's way below NAV and clearly unfair,

but at that point what else could you do? Trust us, we're independent. Vote for us now and we'll take care of

everything. Here's a big document to confuse you. If you can't be bothered, just leave the decisions to us."

I am not impressed by the judgment or independence of those who give this advice - but that's my subjective view;

assessment on the basis of majority voting would be objective, fair and efficient.

Directors giving recommendations should be independent in the normal sense, and not include employees of the aggressor group! See above.

Independent directors should in any case be elected by the independent shareholders. The only "independent" director up for reelection at the last AGM was rejected by 93% of the independent votes cast, but returned anyway thanks to the controlling shareholder.

In the 2016 General Offer, this mattered less, because shareholders could choose to ignore both the advice and the low price offered. This time, we are at risk from the actions and inaction of others. If directors represent themselves as independent and advise soothingly that investors should act against their own interests, this imperils not only those who believe them, but all of the independent shareholders.

In sum

Fincantieri is trying to take Vard private on the cheap at the bottom of the cycle.

They

should bid a fair price, and achieve their goals by persuasion, not force. We hope that Vard investors will

vote in large numbers, that Fincantieri will respect the independent shareholders by abstaining from voting, and

that the shares remain listed. We also hope that writing about this particular case may assist in improving

market

practice for the future, and submit these proposals as our small contribution to that discussion.

Claire Barnes, 15 April 2018, edited and slightly revised 16-20 April

Significant corrections, additions and notes 16-20 Apr:

| Home | Investment philosophy | Fund performance | Reports & articles | *What's new?* |

| Why Apollo? | Who's Claire Barnes? | Fund structure | Poetry & doggerel | Contacts |

{kind=link}