Apollo Asia Fund's NAV rose 2.3% in the fourth quarter, to US$2,099.66 (Series A shares). It was up 4.6% for the year, despite many political and environmental shocks. It was a year in which we completed our exit from four holdings in which we had lost confidence, but in all cases had started trimming earlier, so the positions were no longer large, and portfolio turnover was unprecedentedly low at 2%. In 2019 we added only one new name to the portfolio; it is likely that we'll make rather more changes in the year ahead.

|

|

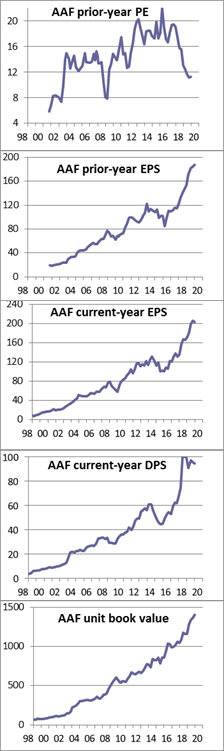

Given the lacklustre NAV performance of recent years, investors may be reassured to see that this is partly because of a significant derating, and that the underlying performance of our portfolio companies has continued to make steady progress. The first chart shows the PE of the current portfolio, based on the reported earnings of each company's last complete financial year. Normally we focus more on current-year earnings, but given higher-than-usual uncertainties of forecasting, it seems more appropriate to start with a measure firmly anchored in historic fact. After upward rerating in the easy-money era, the historic PE has come down to a much more attractive figure of 11.

We will not this time show the PE chart based on estimated current-year earnings, but it shows a similar pattern and derating. As at end-Dec, the estimated current-year earnings multiple was a little over 10. Despite swings and roundabouts, this reflects aggregate EPS growth of 9% for the current portfolio companies.

Historic earnings, dividends and book value per portfolio share are affected not just by the underlying performance of the companies, but by the portfolio weightings and their changes over time. If we trim our holding in a high-PE company and reinvest by adding to a cheaper one, this boosts portfolio EPS. We do not target this effect, and nor do we invest based on mechanistic yardsticks, but over the last three years the per-share earnings and dividends of the portfolio have outpaced those of the average holding, and have grown by about 20% pa.

The upward march of underlying value on several different measures is encouraging - and quite surprising, given the wide variety of new risks encountered over the last few years. One factor is the growth in our weighting of relatively cheap Vietnamese companies. We should not assume continuation of such a pace, but are glad to note the strong growth in the recent past, and the moderate current valuation. Many challenges lie ahead, but some risks are now in the price, and the improved valuation allows us to be more relaxed about the ongoing investment outlook.

We wish all our fellow investors fair sailing and a pirate-free passage over the decade ahead.

Claire Barnes, 17 Jan 2020

| Home | Investment philosophy | Fund performance | Reports & articles | *What's new?* |

| Why Apollo? | Who's Claire Barnes? | Fund structure | Poetry & doggerel | Contacts |