NAV of the Apollo Asia Fund rose 1.3% in the fourth quarter, touching a new high in October. It ended the year at US$2,794.11 (Series A): up 17.6% in one year and 33% over two years, and 74% from the end of March 2020 when markets were beginning to rally after the initial pandemic slump.

|

At the time of our last quarterly report we had just received an opportunistic takeover offer for Malaysia's flexible packaging champion, Daibochi, and wrote about our disappointment with the controlling shareholder Scientex for using the threat of squeeze-out delisting to scare minorities into selling cheaply. The offer lapsed in November, and the direct cost to Daibochi shareholders of responding to it is said to have been RM250,000. At that point, water under the bridge, we congratulated Scientex on having acquired an additional 10% and expressed the hope that we could all focus again on the growth opportunities for the business. We were shocked by an immediate proposal for a bizarrely-chosen name change, and a dramatic shift away from the investor-friendly attitudes and transparency which stood the company in such good stead for the last decade. So once again we have just been writing about the company, ahead of the AGM and after; more will follow once the full Q&A is reported.

We like to invest for the long term in businesses that treat all shareholders as partners, so the apparent change in attitude by Scientex and the Daibochi directors is disconcerting. Directors used to have to face shareholders at least once a year, look them in the eye, and engage in dialogue. The shift online has presented opportunities to curb discussion in favour of monologue; we are grateful to all the management teams who have resisted such temptations, and who see technology as an opportunity to bridge distances and communicate effectively with a larger number of their investors. It is good that regulators are asking for feedback on virtual meetings, since efficient capital allocation depends on the depth and accuracy of investor understanding as well as on governance formalities; constructive engagement between stakeholders seems important to society.

The quarter saw moves towards 'living with Covid' and the relaxation of movement and travel restrictions in several countries, until the Omicron variant complicated things considerably. Within Asia, Hong Kong is in a particularly difficult position. A Bloomberg article explains how 'Hong Kong faces worst of both worlds as Omicron ruins Covid Zero', while its people simultaneously come to terms with rapid deglobalisation and the changes in society following China's crackdown. Press coverage dwindled further, with Citizen News closing on the view that it could no longer report effectively and had to worry about safety of staff given the many arrests and detentions and the lack of clarity on legal boundaries. Hong Kong Free Press, fortunately still operating, provided a helpful summary of changes affecting press freedom since the National Security Law came into effect in July 2020.¹ A lot has changed in eighteen months. This is a problem for investors as well as for governance, since the free flow of information is the lifeblood of markets and of the discussion required for effective responses to changing circumstances.

Unusual weather and rare or unprecedented disasters seem incresingly frequent - severe flooding for example affected Germany in the third quarter, and Malaysia in the fourth - yet the COP26 climate change conference reached no agreeement. Around the world, it seems likely that an increasing proportion of GDP is spent on the mitigation of illth (disaster repairs to infrastructure, countering toxicity, emergency responses), rather than on activities that nurture broad future prosperity (such as the development of relevant skills). The shortcomings of GDP as a measure are widely recognised, but I have not noticed the emergence of more appropriate national policy goals or yardsticks, and would be interested to hear of any progress at country level. Local and individual initiatives hold promise, but may be hampered by non-alignment of national goals and regulations, evolved in different circumstances.

The pandemic has provided disconcerting psychological insights. Given the divergence in attitudes towards relatively simple concepts and practices (such as "airborne" and masking), and inflexibility when dealing with uncertainty, new evidence and prior positions, how are human societies going to deal with more complex issues? Leadership and trust make a big difference. A rational policy with coercion can work too, but an openness to feedback improves the likelihood that the response will remain rational, adapting effectively to changing circumstances. Many Asian countries have done relatively well so far on the public health front, but may find it equally difficult to forge a coherent response to the growing ecological crises.

That matters, because blowback from environmental disruption is biting us harder every year. In the past, investors often ignored limits to economic growth, assuming that substitution and price mechanisms would cause market-based adjustment to all scarcities; limits were acknowledged in theory, but in practice regarded as an issue for future generations (in career terms at least). Then it became clear that we'd moved closer to crunchpoints, likely to be relevant within pension-fund time horizons - but still discounted in net-present-value calculations, so that in practice investment allocation procedure did not change. Now we're learning anew about the fragility of life and of human constructs - and if so much can change in two years (and in one; Myanmar remains a tragedy), what more in the next five?

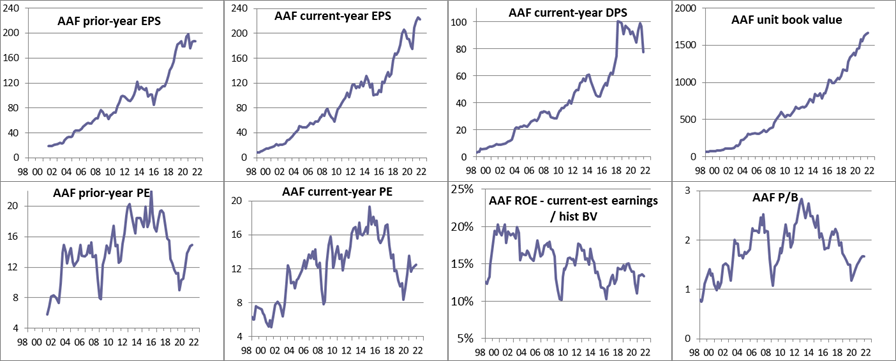

And given all these uncertainties, what should we do about it? Reader ideas would be very welcome. Meanwhile we muddle through, and thanks to a large element of luck, our portfolio of business interests has performed remarkably well. The "prior-year" figures below are for the last full financial year reported, which for many of our companies is calendar 2020; "current year" means the next full year to be reported, with a batch relating to y/e Dec 2021. Some government subsidies in the first pandemic year were withdrawn in the second, and all kinds of crises have been experienced in both years, so our estimates may not be accurate for 2021, let alone further ahead; readers may wish to focus on the prior-year figures and book value. It comes as a pleasant surprise that portfolio earnings and book value have broadly, so far, continued their upward march. We have no great confidence that this can continue, and readers with ideas for a Plan are welcome to send suggestions - but this is the current snapshot, and valuations of our companies are not particularly stretched by past standards.

|

|

Claire Barnes, 10 January 2022

| Home | Investment philosophy | Fund performance | Reports & articles | *What's new?* |

| Why Apollo? | Who's Claire Barnes? | Fund structure | Poetry & doggerel | Contacts |