Giordano shareholders, our company is under attack: please ensure that you vote at the Special General Meeting on 3rd April. Other readers, please help us to spread the word, about the importance of the vote and the interesting situation now emerging.

The Chow Tai Fook group (CTF), controlled by Henry Cheng, made a lowball bid for the company in 2022. It had made its bid conditional on reaching a shareholding over 50%, and did not, so the bid lapsed with no change in its ownership. Now it seeks control without paying at all, through resolutions to oust CEO Peter Lau and appoint four new directors to the board. (It now has 2 of 8 directors; its proposals would give it 6 appointees on a board of 11.)

CTF has not deigned to explain a rationale, and it is hard to imagine that any independent investor would vote to disrupt a company with corporate governance and business performance among the best in Hong Kong on the say-so of a group with a much less impressive track record. Also, why the urgency? This inevitably raises fears that it may wish to divert Giordano's strong cash flows and resources into ventures of its own choosing.

CTF will be allowed to vote its 24% stake, and may be counting on a low turnout, or on sympathetic parties yet to be identified. High turnouts in corporate voting are hard to achieve, but may be vital here to defend an attractive business.

Giordano's strong performance has sometimes been overlooked, because the share price along tells only part of the story: its tight control of working capital has allowed an unusually high payout ratio and it is therefore essential to look at the total return. (This chart shows the contrast.) An investor who subscribed $1,000 on the first day of trading and reinvested all dividends would today have $25,949, representing compound annual growth of 10.4%. By contrast, CTF's flagship company New World Development made a total return of 14% over the 33 years since Giordano's listing, a CAGR of just 0.4%.

Giordano's returns over long periods are highly respectable, but less impressive than its underlying profit and cashflow performance, due to derating.

The company is modest to a fault, and has assumed that its performance speaks for itself. Actually markets are not always efficient, brokers take more interest in the companies that need to raise capital than in those that self-finance their expansion, and investors are swamped with information but may not have access to the most relevant. IR makes a difference.

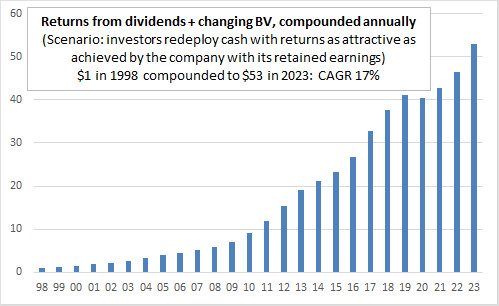

However, the underlying performance has been excellent, and one measure of this is the growth in book value plus dividends per share. As investors, we cannot usually reinvest our dividends at book value in the same company, but we are happy to receive dividends for redeployment. This is a good measure of the returns achieved by the company on the capital under its stewardship. Calculated annually and compounded, the CAGR over the last quarter-century has been 17%. Over the 20 years to 2018, it was 20%; over the last five and four years it has been 7%. (The five years period includes the Hong Kong street protests of 2019, followed by four years with COVID disruption.)

Moreover, in these years of adversity the company may have strengthened its position. Its working capital discipline and financial controls enabled it to ride out border controls and logistical upheaval better than many competitors. Meanwhile it has expanded in India and in Africa, new markets with the potential to become substantial. It is doing so prudently, controlling risk, in the same way that it developed first Southeast Asia, and then the Middle East, as substantial contributors to the business. 80% of operating profits are now generated outside Greater China.

Garment retail is tricky, but Giordano has made a loss in only one of the 33 years since IPO (Covid-year-1), and has never omitted a dividend. It supplies affordable everyday clothing to a wide range of consumers in some of the world's most promising markets. It does so through online channels and many small shops which could complement the urban footprint of other chains: might it now be of interest to a bidder such as Uniqlo? (Uniqlo's parent Fast Retailing, 9983 JP, has a trailing PE of 44 and expected dividend yield of 0.7% per Bloomberg, whereas Giordano is on a historic PE of 10 and dividend yield of 14.0%, with higher growth forecast.) Or to disciplined financial investors in the mould of Berkshire Hathaway, perhaps based in Hong Kong or Singapore, who would back the expansion plans of the current management team?

A Ming Pao article (English translation) quotes David Webb as believing that CTF wishes to sell its Giordano stake, and that its current manoeuvre is a step to that end.¹ The methodology escapes me, but it may well be true that CTF would be a seller at the "right" price. This is always the case for financial investors, and a stable strategic investor would be good for all stakeholders. An offer at twice the level of CTF's 2022 bid might be a starting point for consideration: 10% above the recent high, on a PE of 15 and dividend yield of 7%. This seems readily justifiable, given the resilience and growth potential of the business. Now that CTF has put the company in play, investors of various types may wish to consider the opportunity.

Claire Barnes, 18 March 2024

| Home | Investment philosophy | Fund performance | Reports & articles | *What's new?* |

| Why Apollo? | Who's Claire Barnes? | Fund structure | Poetry & doggerel | Contacts |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}