To What's new? currently

9 Dec 13:

The NAV of the Apollo Asia Fund rose 0.8% in November, to US$1,964.93; charts.

Burma's famous forests are being rapidly logged and deforested on the pretext of plantation development, with concessions granted mainly in conflict areas, according to this account in the Irrawaddy of a report from Forest Trends.

Maritime archaeology disrupted as China flexes muscle - a new twist to the clashes in the South China Sea. The New York Times recently published an atmospheric multimedia account of the Filipino front line, with excellent maps: 'A game of shark and minnow'.

1 Nov 13:

The NAV of the Apollo Asia Fund rose 2.8% in October, to US$1,949.83; charts.

28 Oct 13:

This account of a Pacific voyage reports a frightening loss of fauna, and pollution on a scale

I had never imagined:

'The ocean

is broken'.

3 Oct 13:

The 3Q report discusses overcomplexity and dysfunctionality; also

why we have been selling some of our longstanding holdings, and the resilience we are seeking.

2 Oct 13:

The NAV of the Apollo Asia Fund rose 3.9% in September, to US$1,896.80, 5.3% below the May peak;

charts.

6 Sep 13:

Petronas has added financial statements to its annual reports, back to y/e Mar08, and

published

them on its website. (We don't know when, but the website used to provide just the text.)

Its revenue in 2012 was RM291bn, and capex RM46bn. It contributed RM80bn to federal and state

governments, plus RM2bn to the National Trust Fund: together, 45% of consolidated government revenue.

Income foregone due to the controlled price of gas was RM18.4bn, with this subsidy split between

the power sector (RM10.3bn) and industrial users. The impact of the oil and gas

windfall on the Malaysian economy over the last few decades is immense - and the energy surplus

is now dwindling. A fully-informed debate on national priorities is long overdue, and reporting

a welcome first step.

3 Sep 13:

The NAV of the Apollo Asia Fund fell 5.1% in August, to US$1,824.90;

charts. The big hits came in Thailand, where the US$

value of our holdings fell 16%, with individual stocks down by between 14% and 21%;

Malaysia (-7%); and Japan (-9%). The worst-affected stocks included some of the

high-quality consumer stocks and high-growth consumer finance plays which have been

popular in recent years.

2 Sep 13:

Two excellent postings on

http://cgmalaysia.blogspot.com

summarise the current debate on China Minzhong, the latest S-chip to tumble

on publication of short-seller research. Lots of good reading in the Glaucus

report and links - and in the Wikipedia entry on

Glaucus atlanticus.

2 Aug 13:

The NAV of the Apollo Asia Fund rose 0.6% in July, to US$1,922.43;

charts.

29 Jul 13:

'KL Kepong

implicated in horrific allegations in Indonesian plantations' notes CG Malaysia: do also read

the underlying report by Bloomberg Businessweek, 'Indonesia's palm oil industry rife with human-rights abuses'. The latter reports

attempts by KLK over the last three years to tighten its supply chain and move to direct hiring:

it would be good to hear from the company on the progress and challenges. There are many questions

here for discussion with the managers of plantation and mining groups.

7 Jul 13:

The 2Q report has been posted.

2 Jul 13:

The NAV of the Apollo Asia Fund fell 4.5% in June, to US$1,911.46;

charts.

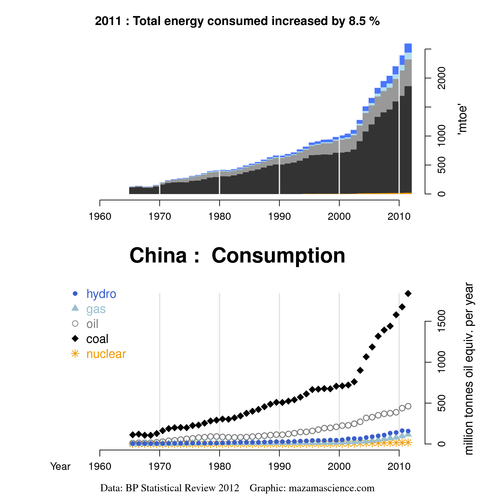

10 Jun 13:

Gail Tverberg has noticed a flattening of per-capita oil consumption in China

and India over the last two years: 'High

oil prices are starting to affect China and India'. The figures for China may reflect its huge

investment in gas pipelines (some splendid charts have been assembled by Phil Ebersole in

'The

geography of pipelinistan)', and in nuclear and renewables, as well as the rising percentage

of coal in its energy mix (shown in

this chart from

the useful Energy Export Databrowser).

However, the statistics are interesting, and both articles recommended.

4 Jun 13:

The NAV of the Apollo Asia Fund rose 2.1% in May, to US$2,002.54; a glance at the

charts should warn our investors to be prepared for

significant retracement.

27 May 13:

In the 1Q report we wrote about Aeon Stores (HK),

now facing competition from its Japanese parent in its home territory of Guangdong,

after decades of investment in that market. Meanwhile, the listed company is

apparently unable to find good uses for its growing cash balance, which at year-end

exceeded shareholders' funds. Given all the efforts by minority shareholders to engage,

we hoped to hear a clearly articulated strategy and appropriate discussion at the AGM -

but the chairman did not bother to attend, no formal time was allotted for discussion or

questions, and the independent directors said that their interest was only in compliance

with HKEX rules. Such apparent lack of concern for minority shareholders may be one

reason why the shares have fallen 26% since the competing investment was announced in January.

25 May 13:

'Walking Beijing's Waterways', a series of short videos by D J Clark

for China Daily, is also

on YouTube (maybe easier to

view), with maps

here. Building on the excellent website 'Beijing's Forgotten Waterways'

(www.hultengren.com/beijing/Rivers/welcome.html

with more detail at

www.hultengren.com - Beijing rivers),

it's a great introduction to the lakes, rivers and canals that are key to the history and geography of

the city - and to the contrasts of life in modern Beijing.

20 May 13:

Extraordinary reading from Fortune magazine:

'Dirty

medicine: the epic inside story of long-term criminal fraud at Ranbaxy'. The author

appears to have been following the industry, and this story, for a long time: see

katherineeban.com. An earlier article discusses

increasing

questions over the efficacy of some generic drugs.

6 May 13:

The Malaysian public is to be congratulated on the 80% turnout in

yesterday's General Election. Electoral irregularities have been

a feature in past elections, but never previously

documented

in such detail, and never before in an election which has been so

closely fought. Despite the huge advantages and biases of incumbency,

the opposition coalition appears to have won the popular vote - so the

impact of additional votes could well have tipped the balance. Bersih, the Coalition

for Clean and Fair Elections, is protesting many alleged

irregularities. Clean and fair elections are a

reasonable

expectation, not to be confused with sedition, and would free up energy

to focus on the real policy challenges of the future.

A tale of two very different reports, and the preference of the international community for the palatable version (see penultimate paragraph): 'Myanmar whitewashes ethnic cleansing'. The Human Rights Watch report is available here.

2 May 13:

The NAV of the Apollo Asia Fund rose 1.4% in April, to US$1,961.78;

charts.

12 Apr 13:

Sarawak Report has been down for two days after a major

cyber-attack. Distributed denial of service (DDoS) attacks have

reached

unprecedented scale recently. We found cached versions of Sarawak Report articles

using Tor Browser.

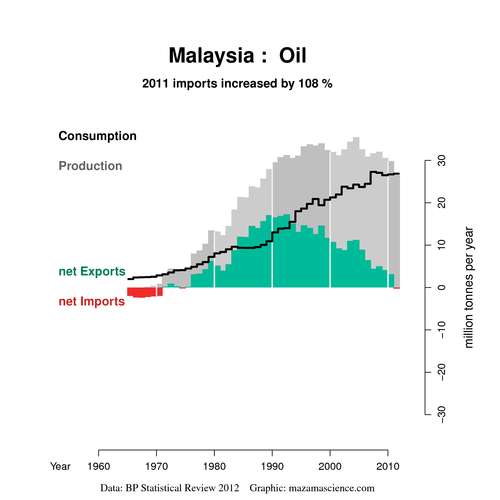

9 Apr 13:

Gail Tverberg examines how

oil exporters reach financial collapse with reference to Egypt, Syria, Yemen, Argentina, Venezuela, the USSR,

and in the comments Bahrain. One country not mentioned is Malaysia.

This chart from the

Energy Export Databrowser has been shown

before: the picture of rising consumption overtaking declining domestic production was

discussed in our 2Q12 report. Like the other countries mentioned,

Malaysia has other resources, but the oil windfall has been a major contributor to its

recent prosperity and government finances. The same is true of the UK, so Malaysians

buying London property may not be diversifying as effectively as they think.

6 Apr 13:

The 1Q report has been posted.

4 Apr 13:

Last year the strange bond issue

for 1MDB Energy caused us to wonder about Malaysia's off-balance-sheet

debt. Kinibiz has written a series of

articles about 1Malaysia Development Berhad, concluding that

'1MDBs cloak and dagger style of operation with many unanswered questions

and dubious dealing is very unbecoming of a sovereign fund that is

supposed to to make strategic investments that will be of value to the country',

and posing

10

pressing questions for 1MDB.

2 Apr 13:

The NAV of the Apollo Asia Fund rose 0.7% in March, to US$1,935.60;

charts.

29 Mar 13:

Efficient capital allocation is so important that stock exchanges should be

run in the public interest. In practice, ownership by member brokers often

worked quite well.

Running stock exchanges for profit sets up huge conflicts of interest. I have

noted some of these in the past. Others are clearly explained in this article

on

Bursa CEO pay and lack of retail investors.

Stock exchanges are too important to be listed companies!

8 Mar 13:

Fascinating insights into the conflicts of interest in business

programming for western television accompany the exposure of the Malaysian

government's payments for

positive coverage. More here (and much more in that site's archives).

4 Mar 13:

The NAV of the Apollo Asia Fund rose 3.6% in February, to US$1,922.49;

charts.

16 Feb 13:

Webb-site's HKID Index service has been suspended; David Webb explains why this is

a dark day day for

transparency in Hong Kong.

7 Feb 13:

Asia Pulp & Paper (APP) has announced a new forest conservation policy suspending all clearance

of natural forest by APP and its suppliers.

This would be

an

extraordinary turnaround given the group's history.

According to the company:

'Recent independent assessments of the growth and yields of APP suppliers'

plantation areas confirms that the company has sufficient plantation

resources to meet the long term forecast demand for its pulp mills.' We call

for all relevant data to be periodically published, to allow independent

verification by parties other than company-appointed consultants.

6 Feb 13:

The NAV of the Apollo Asia Fund rose 2.8% in January, to US$1,855.67;

charts.

ACSA withdrew the proposal to make a large loan to its parent. The group wishes to expand rapidly in China; if this is now belatedly permitted, the opportunities there could be large in relation to the mature profitable Hong Kong business. The company tells us that it intended to allow the ACSA investors to participate without over-burdening the P&L, and is now considering structures to bring greater clarity to the allocation of new investments while avoiding conflicts of interest.

23 Jan 13:

A helpful investor has noted that unless Aeon Credit Service Asia

(ACSA) could rely on unanimous shareholder approval (which it

clearly cannot, as we object strongly), its proposal appears to be

in breach of section

168A of the Companies Ordinance in Hong Kong,

as the loan would be financing a competitor. We have written further

to the company, urging it to withdraw the proposal, and to rethink

its plans in China to avoid conflicts of interest and ensure fair

treatment of minority shareholders.

Michiel Wind has commented on the Aeon Credit case and the case of Panasonic Manufacturing Malaysia, which has 70% of shareholders' funds lent out to a related company. He says 'lending money to a related company is a no-no' and that 'Japanese companies should welcome good, internationally accepted, corporate governance practices, it is long overdue.'

22 Jan 13:

Another formerly-reputable multinational is behaving badly, and this

time we own it. David Webb asks shareholders to

veto Aeon Credit

loan to parent. We have written to the company to support his

call to withdraw the proposal, pay a special dividend, and remove

conflicts of interest. We told them that we were astonished to read

the proposal for ACH (the parent) to develop its own China business

in competition with ACSA (the listed company), and appalled to read

that it proposes to fund this with ACSA's money. We noted that many of ACSA's

minority shareholders stuck with ACSA shares over the years despite

recurrent disappointments over more than a decade as to the timing of

China business development, in the expectation of an eventual reward

for their patience. Minority shareholders deserve better than this!

All Hong Kong investors should read the webb-site article - and all

shareholders, please vote.

A Global Witness report in 2012 highlighted HSBC's ongoing relationships with several companies whose reputations sit very oddly with HSBC's professed environmental policy. (See post of 21Nov.) Masya Spek explains why HSBC's forest policy is not working, and suggests how to tighten it, including disclosure-based principles that may also be helpful to other stakeholders: Gaps in the canopy: suggestions for HSBC's forest policy.

21 Jan 13:

Energy is a huge issue for Malaysia. Like the UK and Egypt, Malaysia

has benefitted from an enormous energy windfall, which has recently

appeared to be dwindling fast - but the

challenges are barely discussed. Petronas publishes no proper accounts, and

its quarterly reports omit mention of key strategic and operational

issues. Petronas is apparently 'accountable only to the prime

minister of the day, not even to Parliament'. Friday's announcement

by Petronas of an

oil and gas discovery onshore Sarawak

occasioned jubilant press coverage, with talk

of a socio-economic boom for Miri. Given the history of development

and resource theft in Sarawak, suspicions

that the people will see little benefit are all too plausible.

Calls for transparent accounting, and accountability, by Petronas,

state and federal authorities are highly relevant to long-term investors.

Latest in a series on the role of the press in facilitating rumour-driven moves in Malaysian shares: 'Do you think there's honesty and integrity in our financial news?'

16 Jan 13:

The 4Q report has been posted.

4 Jan 13:

The NAV of the Apollo Asia Fund rose 1.8% in December, to US$1,805.72;

charts.

Claire Barnes

To What was new archive - 2012

To What was new archive - 2011

To What was new archive - 2010

To What was new archive - 2009

To What was new archive - 2008

To What was new archive - 2007

To What was new archive - 2006

To What was new archive - 2005

To What was new archive - 2004

To What was new archive - 2003

To What was new archive - 2002

To What was new archive - 2001

To What was new archive - 2000

To What was new archive - 1999

| Home | Investment philosophy | Fund performance | Reports & articles | *What's new?* |

| Why Apollo? | Who's Claire Barnes? | Fund structure | Poetry & doggerel | Contacts |

{kind=link}

{kind=link}