NAV of the Apollo Asia Fund rose 5.5% in the fourth quarter, to US$2,591.18 (Series A). That's down 7.3% year-on-year (compared to a 23% fall for the MSCI all-country Far East ex-Japan index), but up 23% over the three years since the first international alarm for the COVID-19 pandemic. It's up 61% since the end of March 2020, when global markets had begun to rally after the initial pandemic slump. Over the 25 years since inception, compound annual growth has been 17%, and the NAV has multiplied 54-fold.

Asian currencies started to rally in the fourth quarter, after many months of weakening against a surging US$. For the year as a whole, Asian currencies fell 6.4% as measured by ADXY, the Bloomberg JPMorgan Asian Dollar Index, accounting for much of the decline in fund NAV. Since these currency losses are unrealised, there is scope for a future reversal and tailwind.

|

Malaysia again has a legitimate government, after the interesting experience of 2¾ years without. Despite the complexities of an awkward coalition, there is now a welcome sense of purpose and accountability in several ministries, and renewed discussion of policies and options. Your fund has relatively little invested in Malaysia, but the change is a relief to your fund manager.

The period for which China contained COVID infections was also 2¾ years. With the genie now out of the bottle in this last of Asia's bastions, COVID has spread worldwide. It remains to be seen how different countries (and international supply chains) will cope with further waves of sickness and with the long-term consequences of a less healthy population, reduced workforce, and higher rates of disability. The year ended with high COVID mortality in Japan, China and Hong Kong, but the greater concern may be morbidity. The impairment of health and productivity after COVID infections seems to be having a significant economic impact in countries such as the US and UK (beyond crude reductions in the labour force, first to be measured). A new study of Long Covid talks of over 65 million people affected worldwide, with significant numbers unable to return to work, and many facing lifelong disabilities. Hopes of an end to the pandemic were clearly premature, and in many places have discouraged effective mitigation. The insouciance of western governments is disappointing, especially when their decisions influence actions around the world. As investors, gaps between perception and reality are always interesting. They may present opportunities - but the misallocation of a whole society's resources also poses great dangers.

2022 was a year in which many people around the world were shocked by personal experience of climate change: floods, droughts, heatwaves etc. The costs of mitigation and adaptation are rising rapidly¹, and will eventually be distributed across society one way or another; government policymakers are likely to be the targets of ever-more-intense lobbying.

|

The crisis in the natural world has been recognised by the world's governments. The Kunming-Montreal Global Biodiversity Framework, finally agreed on 19 Dec, was a landmark agreement, and reaching consensus in current political conditions was a remarkable achievement. Effective implementation would be far more challenging, and commentators were quick to predict that few governments will make any serious effort. The necessary reimagining of the goals of society is a topic too difficult for most governments to contemplate - but it would be good to try, before change is forced upon us.

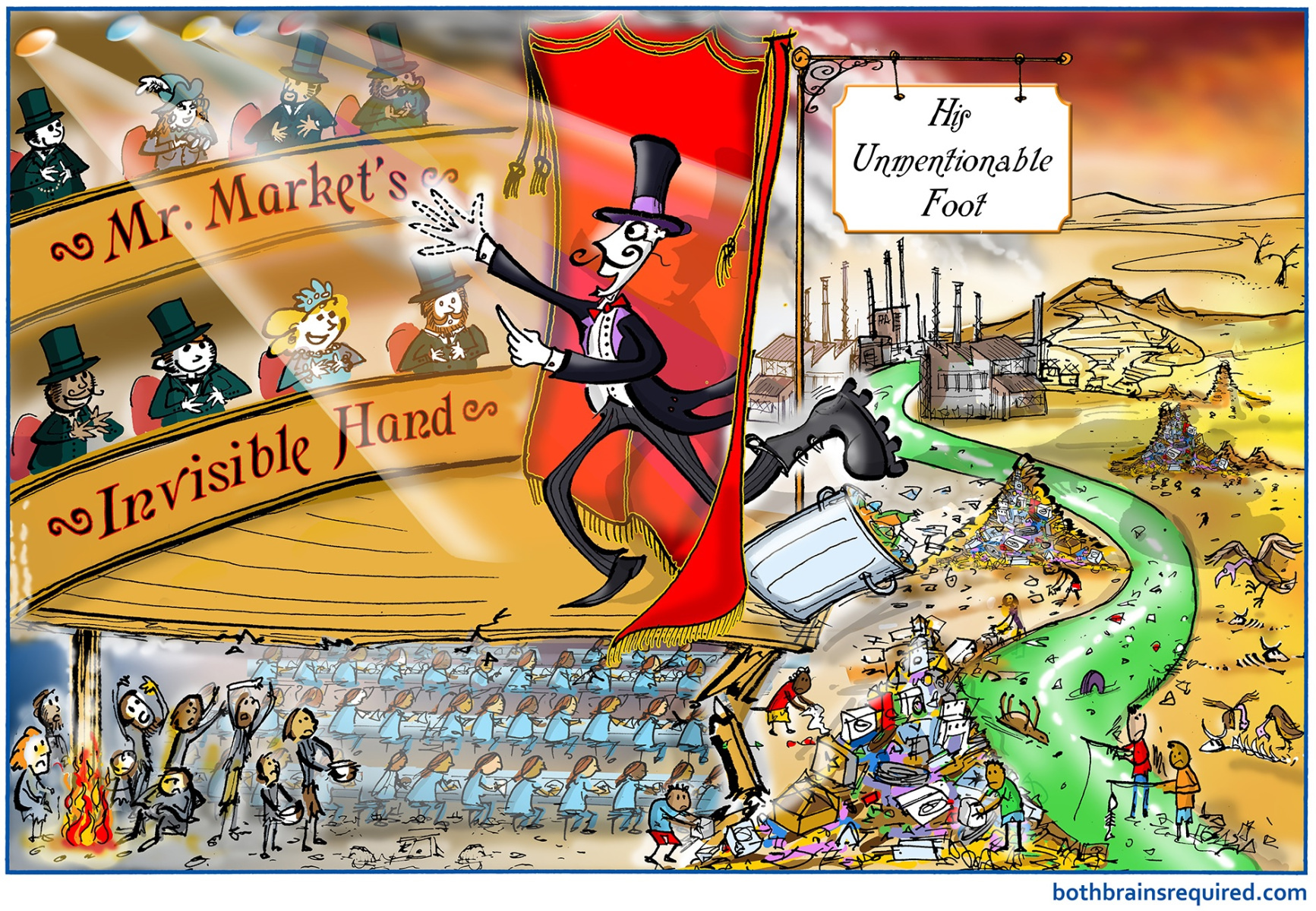

A wonderfully eloquent summary of the need to change old mental models is by Duncan Austin: 'The Towering Problem of Externality-Denying Capitalism'. Do read the full report. His illustrations are invaluable, and free to use. I hope that teachers of economics will henceforth include the Unmentionable Foot.

In 2019, I described the terrifying arithmetic of steady growth in man's material footprint leading to accelerating decline in the natural world. The decline proceeds gradually, and then suddenly, so I dubbed this a Hemingway decline. My model was prompted by observation of the world around me in Malaysia, but the arithmetic is indisputable. The actuary Guy Thomas set out the maths in his article 'Two parts of a whole: compound growth and Hemingway decline'. Guy and I both considered at the time why this simple arithmetical relationship might not be widely appreciated. It prompted little noticeable interest - and Malaysia, like other countries in Asia, continues to track this most unfortunate of models. As I read of catastrophic declines in the numbers of insects, or fish, and of the many sudden extinctions², it seems to me that this simple mathematical insight, the Hemingway Decline, has some explanatory power.³

The world is facing many challenges simultaneously, and one excellent overview is from another actuary, Gail Tverberg. (URLs for her articles usually include the full title, but the URL for this one is unusually succinct). She paints a bleak picture, and I mostly agree - but her analysis also points to the relative advantages of Asia. A comprehensive range of manufacturing skills, capabilities and costpoints; a fairly wide range of natural resources; improved access to energy since the Russian debacle; and the ability to trade with everybody and probably outbid/outmanoeuvre competitors for other inputs. Politics is a wild card, but nowadays where is it not? For investors in the Americas and Europe, an allocation to Asia looks eminently sensible - and the value is better now than a year ago.

The Year of the Tiger certainly lived up to its reputation for upheaval and storms. In a few more days it will be the Year of the Rabbit, traditionally much more peaceful. May calm and good sense prevail, and our readers prosper!

Claire Barnes, 16 January 2023

| Home | Investment philosophy | Fund performance | Reports & articles | *What's new?* |

| Why Apollo? | Who's Claire Barnes? | Fund structure | Poetry & doggerel | Contacts |